Report on The Bioscience and Technology Institute

Session: 2011/2012

Date: 02 May 2012

Reference: NIA 48/11-15

ISBN: 978-0-339-60426-1

Mandate Number: Eighth Report

report-nia-48-11-15.pdf (4.13 mb)

Public Accounts Committee

Report on The Bioscience

and Technology Institute

Together with the Minutes of Proceedings of the Committee

Relating to the Report and the Minutes of Evidence

Ordered by The Public Accounts Committee to be printed 2 May 2012

Report: NIA 48/11-15 Public Accounts Committee

Mandate 2011/15 Eighth Report

Correspondence received post publication

IMPORTANT - PLEASE NOTE:

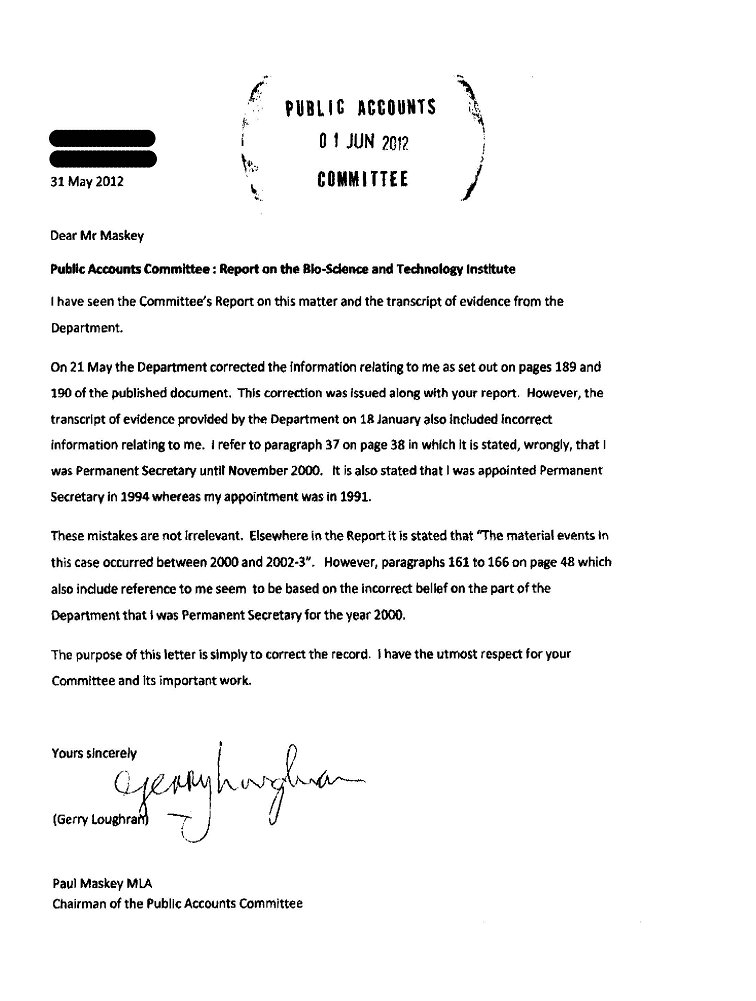

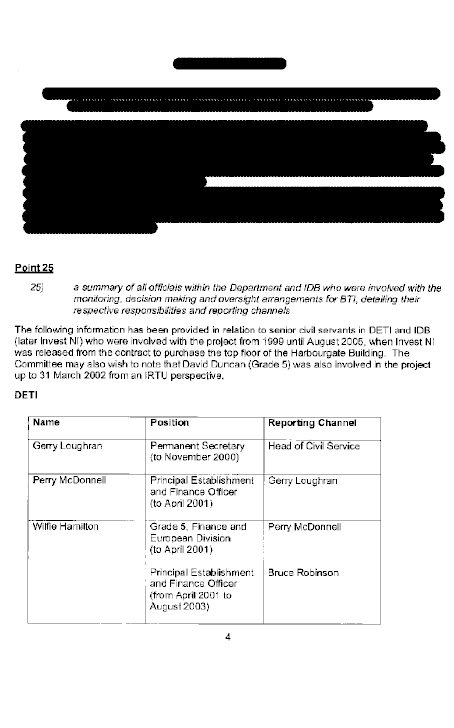

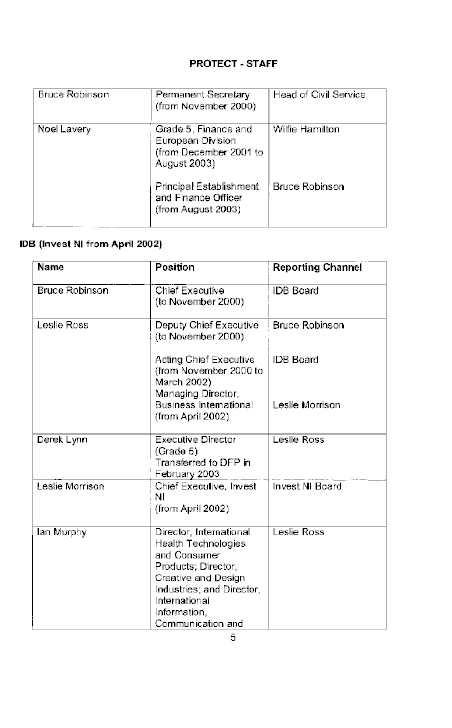

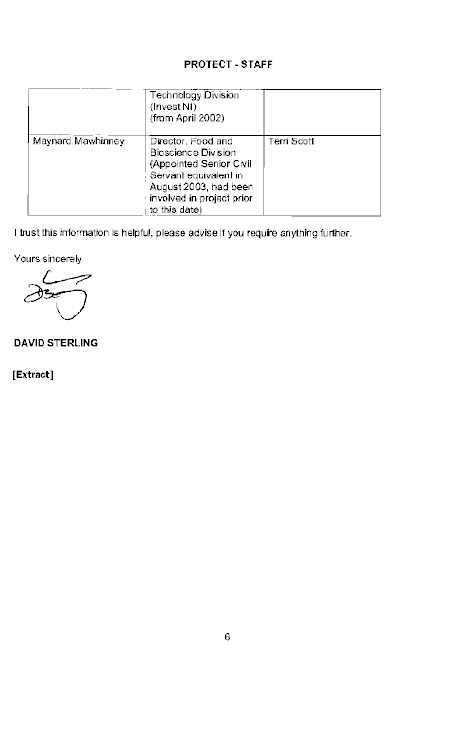

Correspondence received from DETI on 21 May 2012, which should be read in conjunction with pages 15, 189, 190 and Paragraph 47 of the report.

To: Aoibhinn Treanor (Public Accounts Committee Clerk)

From: Trevor Cooper

Date: 21 May 2012

Public Accounts Committee - Draft Report on the Bioscience and Technology Institute

1. Further to our earlier conversation, I am writing to highlight factual inaccuaracies around the information provided in the table on pages 189 and 190. The inaccuaracies relates to the information provided in the table on page 190 on the dates of Bruce Robinson's tenure as Chief Executive of IDB, the omission in the table on page 190 of a period in which Bruce Robinson Acted into the position of DETI Permanent Secretary, and inaccuracy in the dates of tenure of Gerry Loughran as Permanent Secretary of DETI in the table on page 189.

2. As currently drafted the Table on page 190 records Bruce Robinson as Chief Executive of IDB to November 2000. This should record Bruce Robinson as being Chief Executive of IDB to April 2000.

3. The Table on page 190 also records Bruce Robinson as being Permanent Secretary of DETI from November 2000. This table should record a period from May 2000 when Bruce Robinson acted into the position of Permanent Secretary of the Department prior to his substantive appointment in November.

4. As currently drafted the Table on page 189 records Gerry Loughran as permanent Secretary to November 2000. This should be to April 2000.

5. I would like to apologise to the Committee for the need to correct the record on this matter, however the Department believes that it is important that the record be updated on this matter.

Trevor Cooper

Acting Senior Finance Director

Membership

The membership of the Committee since 23 May 2011 has been as follows:

Mr Paul Maskey (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

Mr Adrian McQuillan[1]

Mr Conor Murphy[2]

[1] With effect from 24 October 2011 Mr Adrian McQuillan replaced Mr Paul Frew

[2] With effect from 23 January 2012 Mr Conor Murphy replaced Ms Jennifer McCann

Table of Contents

List of abbreviations used in the Report

REPORT

DETI's Response to the Failings in this Case

The Failure of Leadership within the Department and its Agencies

Appendix 1:

Appendix 2:

Appendix 3:

Appendix 4:

List of Abbreviations used in the Report

C&AG - Comptroller and Auditor General

the Committee - Public Accounts Committee

BTI - Bioscience and Technology Institute Limited

BCH - Belfast City Hospital

DETI/the Department - Department of Enterprise and Investment

IDB - Industrial Development Board

IRTU - Industrial Research Technology Unit

IFI - International Fund for Ireland

Invest NI - Invest Northern Ireland

CARB - Chartered Accountants Regulatory Board

DFP - Department of Finance and Personnel

NICS - Northern Ireland Civil Service

Executive Summary

Introduction

1. This report examines the reasons for the failure of a major innovation project, the Bioscience and Technology Institute Limited (BTI). BTI was incorporated as a not-for-profit company in November 1998. Its primary objective was to provide biotechnology incubator facilities, through the development of a specialist building at Belfast City Hospital (BCH). The company was to be commercially sustained by the rent charged to tenant organisations, primarily early-stage biotechnology companies.

2. The project secured grant of £2.2 million from four funding bodies: the Department of Enterprise Trade and Investment (the Department/DETI); two of its agencies — the Industrial Development Board (IDB), the Industrial Research and Technology Unit (IRTU) — and the International Fund for Ireland (IFI). In addition, loan funding was provided by the bank (initially £1.5 million) and a private donor (£1.2 million).

3. As it transpired, difficulties in progressing the project at BCH, within the required funding timeframe, led to BTI purchasing "Harbourgate", a shell building some four miles away in the Belfast Harbour Estate. In the event, BTI had inadequate funds to complete the fit-out, the costs of which turned out to have been substantially underestimated. As a result, the building never became operational and did not generate any income for BTI.

4. In November 2005, with the company unable to service its loan funding, the bank took possession of Harbourgate and sold it the following month. The sale proceeds of £4.55 million were sufficient to repay BTI's debt to the bank in full, with the surplus used to make a part-payment on the secured debt to the private donor. No moneys were available to pay the other creditors, including the funding bodies. BTI remains technically insolvent and steps are now being taken to begin winding up the company.

Overall conclusions

5. The Bioscience case is one of the starkest examples of incompetence and mismanagement that this Committee has ever examined and stands as a lesson in how not to manage a major innovation project. As such, it is a damning indictment of the capabilities within the Department and its agencies, at that time, to oversee a new development project.

6. It would be difficult to overstate just how badly this project was handled, both by the funding bodies and by the BTI Board itself. From beginning to end, the Committee noted a catalogue of negligence and ineptitude, the nature and extent of which could only be described as staggering. Well established procedures, underpinning the proper conduct of public business, were blatantly ignored; and key lessons from earlier failures were not taken on board.

7. There are many aspects of the way in which this project was handled that the Committee finds profoundly disturbing. BTI's corporate governance arrangements were exceptionally weak, with conflicts of interest, in particular, consistently being badly handled. There were several cases of improper behaviour which, the Committee suspects, were fraudulent in intent. One of the most worrying aspects of the project was the repeated failure, at a senior level within both DETI and IDB/Invest NI, to get a firm grip on matters. The Committee's impression is of a management culture, at that time, which acquiesced in ignoring the rules and circumventing their own controls. That is an appalling state of affairs.

8. The Committee is far from convinced that it has got to the bottom of several important issues in this case, especially the circumstances surrounding the acquisition of the Harbourgate building. The lack of transparency around the sourcing of the premises and the negotiation of the purchase price is of particular concern. In the Committee's opinion, the Department must look further into these issues and discuss them in detail with the PSNI, to determine whether any criminal activity may have taken place.

9. There is also a worrying lack of documentary evidence in a number of areas, most notably around IDB's consideration and approval of funding for BTI. Indeed, it is of particular concern that at least one file was destroyed by Invest NI, some four months after it had been requested for examination by the Company Inspectors. Moreover, the file review form, which evidenced the decision to destroy the file was itself destroyed without trace. This is a most unusual sequence of events. With Invest NI unable to provide a convincing explanation for what had happened, the Committee has a deep sense of unease over this issue and is concerned that there may have been a deliberate cover-up.

The management of risk

10. The Committee has noted the assurances from both the Department and Invest NI that lessons have been learned and that controls are better today than 10 years ago. While these assurances are welcome, it must not be forgotten that most of the shortcomings in this case stemmed from a failure to apply existing controls, rather than an absence of controls.

11. The Committee would like to emphasise that it does not want the Department and Invest NI to operate as risk-averse organisations. The Committee supports risk-taking in appropriate circumstances, but only where it is properly assessed and effectively managed. The Committee recognises that supporting new and innovative projects is a risk business and that difficult judgements have to be made. It also accepts that some projects are likely to fail. However, the Department's operational guidelines and the lessons from the past are key elements of the risk assessment and management process and must never be ignored or sidestepped.

The adequacy of DETI's response to the failings in this case

12. The Committee has serious concerns about the way in which the Department responded to its suspicions of fraud and impropriety. Overall, it adopted a piecemeal approach, particularly in its consultations with the PSNI. In the Committee's view, matters should have been dealt with holistically, with DETI formally consulting the PSNI on all matters of concern after completion of the Company Inspectors' report. Fraud and impropriety, whether actual or attempted, are serious issues which this Committee expects departments to address comprehensively and professionally, not in the haphazard fashion so evident in this case.

13. The Department commissioned an independent review of the conduct of officials involved in the BTI case, and this resulted in disciplinary action being taken by Invest NI against two of its officers, in February 2011. Given the significance of breach of IDB procedures, the Committee finds it hard to accept that disciplinary proceedings against the former IDB Chief Executive were deemed not to be warranted. While the Department is to be commended for instigating a disciplinary process, the Committee has a concern about the extent to which that process was applied. The conduct of only four officials was examined, whereas the failings in this case ranged much more widely. The Committee notes the Accounting Officer's explanation that the disciplinary review did not consider the conduct of retired departmental and Invest NI employees, because they are now effectively beyond the reach of the disciplinary processes.

14. In the Committee's view, it is most unfortunate that several of those senior officials seemingly most culpable for the shortcomings in this case could not be subject to a disciplinary investigation, by virtue of their having retired from the public sector. This renders the outcome of the disciplinary process less than satisfactory. The Civil Service needs to look at ways in which disciplinary issues, in cases like BTI, can be dealt with much more urgently.

The failure of leadership within DETI and its agencies

15. One of the issues which the Committee has found most disturbing in the BTI project is the extent to which some of the most senior officials in both DETI and IDB/Invest NI were apparently complicit in the many failings that occurred. The Committee acknowledges that the effective oversight of a major new innovation project presents many challenges. But it is precisely because of the numerous risks involved that the successful handling of such a project requires not only the highest standards of administration but a commensurate standard of leadership.

16. One of the most important messages coming out of this report, therefore, is to stress the particular onus on an organisation's top management to ensure that control procedures are followed and that the ethos of their organisation is fully in keeping with the proper conduct of public business. The Committee notes the work being done within Invest NI by the current Chief Executive through his 'Transform' programme of change and commends him for this initiative. It is important that both Invest NI and DETI now consider how the lessons from the BTI project can best be assimilated within their own organisations.

Project Outcomes

17. The Committee is extremely disappointed with the outcomes of this project. Through a combination of apathy, incompetence and a disregard for proper administration, the bioscience research and incubation facility was never established. As a result, an initiative that promised so much and which should have been a major success story for Northern Ireland was instead transformed into an unmitigated failure.

18. In view of the project failing to achieve any of its objectives, the Committee can only conclude that it provided no value for the public funds committed to it. With no sums having been recovered by Government, some £2.2 million of taxpayers' money has been totally wasted. In addition, over £1 million is also left owing to the estate of the private donor and a further £0.4 million is owed to HM Revenue and Customs. This is a devastating ending to a venture that had so much potential.

Summary of Recommendations

Recommendation 1

1. The Committee recommends that the Department and Invest NI ensure that their guidelines on project appraisal and approval are rigorously applied, in all cases. Ignoring well-established appraisal and approval procedures only serves to add unnecessary risk to the management of projects.

Recommendation 2

2. The Committee recommends that the Department and Invest NI revise their guidelines to ensure that selective financial assistance is not offered, even on a heavily conditional basis, to a project with a poorly developed business plan.

Recommendation 3

3. The destruction of documents in a case which is subject to a statutory investigation is wholly unacceptable. The Committee recommends that the Department satisfies itself as to the adequacy of Invest NI's file and electronic records management and retention protocols and their effective implementation.

Recommendation 4

4. The conditions and prior conditions included in letters of offer are a direct response to the risks assessed at appraisal. The Committee recommends that any proposal to change those conditions, which significantly increases the risk to the funder, should be subjected to a formal re-appraisal before the decision is made.

Recommendation 5

5. The Committee recommends that DETI and Invest NI take steps to ensure that decisions to pay grant are not driven solely by the need to meet funding deadlines. While the Committee readily acknowledges the importance of such deadlines, no payment should be made if the provision of grant cannot otherwise be fully justified.

Recommendation 6

6. The Committee recommends that DETI and Invest NI review their project monitoring procedures to take on board the lessons from the BTI case. Grant-aided projects must always be actively monitored; where information provided by an assisted body is deficient, or indicates that the project is not proceeding to plan, this must be quickly addressed, including where necessary, a re-appraisal of the project.

Recommendation 7

7. When providing substantial sums of financial assistance to organisations like BTI, DETI and Invest NI must ensure that comprehensive corporate governance structures are in place and are fully functional when the project starts. This must include ensuring that the Board itself possesses the appropriate range and level of skills and experience.

Recommendation 8

8. Bypassing agreed payment authorisation procedures and failing to ensure that conditions of offer have been met are serious breaches of control. The Committee recommends that the Department ensures its arrangements for releasing grants to projects are sufficiently rigorous to prevent payments being made until all relevant checks have been satisfactorily completed and all conditions of offer complied with.

Recommendation 9

9. The Committee is critical of the haphazard way in which DETI responded to the suspicions of fraud and impropriety in this case, particularly in its consultations with the PSNI. The Committee recommends, therefore, that DETI reviews the adequacy of its fraud response plan, considers whether additional training is required for staff charged with handling fraud cases, and reports back to the Committee with its conclusions and recommendations for improvement.

Recommendation 10

10. The Committee recommends that DETI rigorously investigates the circumstances surrounding the sourcing of the Harbourgate building and negotiation of the purchase price, and then consults with the PSNI to determine whether any criminal actions may have taken place, and informs the Committee of the outcome.

Recommendation 11

11. The Committee recommends that DETI and DFP ensure that future referrals to professional bodies are processed on a much more timely basis and that the substance of the complaint is fully and clearly articulated.

Recommendation 12

12. The Committee recommends that DETI clarifies with the Law Society the rationale behind its decision to accept the explanation of BTI's solicitor.

Recommendation 13

13. The Committee recommends that the Civil Service ensures that disciplinary issues, in cases like BTI, can be dealt with much more urgently.

Recommendation 14

14. There is a particular responsibility on top management to encourage a culture of compliance with good practice throughout their organisation. The Committee recommends that both DETI and Invest NI now ensure that the lessons on leadership and management culture arising from this report can best be assimilated within their respective organisations.

Introduction

1. The Public Accounts Committee met on 18 January 2012 to consider the Comptroller and Auditor General's report on 'DETI: The Bioscience and Technology Centre', (29 November 2011). The witnesses were:

- Mr David Sterling, Accounting Officer, Department of Enterprise, Trade and Investment (DETI);

- Mr Alastair Hamilton, Chief Executive, Invest Northern Ireland (Invest NI);

- Mr Mel Chittock, Director of Finance and Internal Operations, Invest NI;

- Mr Trevor Cooper, Director of Finance, DETI;

- Mr Kieran Donnelly, Comptroller and Auditor General;

- Ms Fiona Hamill, Treasury Officer of Accounts.

The Committee wrote to Mr Sterling on 27 January 2012 and 5 March with further queries following the evidence session. Mr Sterling replied on 10 and 20 February; 5, 16, 21 and 30 March; and 16 and 26 April 2012.

2. This report examines the reasons for the failure of a major innovation project, the Bioscience and Technology Institute Limited (BTI). BTI was incorporated as a not-for-profit company in November 1998. Its primary objective was to provide biotechnology incubator facilities, through the development of a specialist building at Belfast City Hospital (BCH). The company was to be commercially sustained by the rent charged to tenant organisations, primarily early-stage biotechnology companies. The project secured grant of £2.2 million from four funding bodies — the Department of Enterprise Trade and Investment (the Department/DETI); two of its agencies — the Industrial Development Board (IDB), the Industrial Research and Technology Unit (IRTU); and the International Fund for Ireland (IFI). In addition, loan funding was provided by the bank (initially £1.5 million) and a private donor (£1.2 million).

3. As it transpired, difficulties in progressing the project at BCH, within the required funding timeframe, led to BTI purchasing "Harbourgate", a shell building some four miles away in the Belfast Harbour Estate. In the event, BTI had inadequate funds to complete the fit-out, the costs of which turned out to have been substantially underestimated. As a result, the building never became operational and did not generate any income for BTI. In November 2005, with the company unable to service its loan funding, the bank took possession of Harbourgate and sold it the following month. The sale proceeds of £4.55 million were sufficient to repay BTI's debt to the bank in full, with the surplus used to make a part-payment on the secured debt to the private donor. No monies were available to pay the other creditors, including the funding bodies. BTI remains technically insolvent and steps are now being taken to begin winding up the company.

4. In taking evidence, the Committee focused on four key areas. These were:

- The management of risk;

- The adequacy of DETI's response to the failings in this case;

- The failure of leadership within DETI and its agencies;

- Project outcomes.

The management of risk

Introduction

5. Providing financial support to new, innovative greenfield projects is inherently high risk. Accordingly, Government has devised comprehensive control procedures to help assess and manage that risk. Unfortunately, there was a widespread and repeated failure by the Department and its agencies to apply these well-established procedures to the BTI project.

6. It would be difficult to overstate just how badly this project was handled, both by the funding bodies and by the BTI Board itself. From beginning to end, the Committee noted an appalling catalogue of negligence and ineptitude, the nature and extent of which could only be described as staggering. Procedures underpinning the proper conduct of public business were blatantly ignored and key lessons from earlier failures were not taken on board. The following paragraphs outline the key failings that beset this project over the course of its relatively short lifetime.

Initial Project Appraisal and Offer of Assistance

7. There were a number of significant breaches of controls and poor judgements around the initial appraisal and offer of assistance, which added unnecessarily to the already significant risks of supporting this project:

- IDB accepted a BTI business plan which had not been fully developed, for appraisal. This markedly increased the risk to public funds. Due to various uncertainties in the plan, particularly around sources of private and donor funding and the estimates of costs, a meaningful assessment of the viability of the project was not possible.

- In view of the uncertainties, the Appraisal Report recommended that the promoters be asked to resubmit their proposals. However, this recommendation was ignored and, instead, each of the funders provided a heavily conditioned offer to BTI. For example, IDB's offer included 11 prior conditions. This was quite extraordinary.

- IDB's guidelines required projects seeking financial assistance to be considered by a "Casework Committee". This was a specialist mechanism, designed to provide a comprehensive challenge to the project proposal. Unusually, however, and quite improperly, this control was bypassed, with approval being sought instead from the IDB "Resource Group". This was not the appropriate mechanism and offered a much lower level of scrutiny.

- DETI's offer of funding also required DFP approval. However, DFP's analysis appears to have been unusually weak — despite the reservations of the Appraisal Report and the abnormally high number of prior conditions, DFP approved DETI's decision to offer financial support.

Recommendation 1

8. The Committee recommends that the Department and Invest NI ensure that their guidelines on project appraisal and approval are rigorously applied, in all cases. Ignoring well-established appraisal and approval procedures only serves to add unnecessary risk to the management of projects.

Recommendation 2

9. The Committee recommends that the Department and Invest NI revise their guidelines to ensure that selective financial assistance is not offered, even on a heavily conditional basis, to a project with a poorly developed business plan.

Missing Documentation

10. There is a worrying lack of documentary evidence around IDB's consideration and approval of funding for BTI. As stated above, the process adopted was inappropriate and constituted a serious breach of normal operating procedures. While trying to shed more light on this, the Company Inspectors were repeatedly unable to access several of the IDB Resource Group files. Astonishingly, one of these files was then destroyed by Invest NI, some four months after it had been requested for examination by the Company Inspectors. Moreover, the file review form, which evidenced the decision to destroy the file, was itself destroyed without trace.

11. This is a most unusual sequence of events and raises suspicions that papers might have been destroyed to intentionally remove evidence. Although Invest NI said that there is no evidence that there had been a purposeful and wilful destruction of the file, they were unable to provide a convincing explanation for what had happened. As a result, the Committee has a deep sense of unease over this issue and is concerned that there may have been a deliberate cover-up.

Recommendation 3

12. The destruction of documents in a case which is subject to a statutory investigation is wholly unacceptable. The Committee recommends that the Department satisfies itself as to the adequacy of Invest NI's file and electronic records management and retention protocols and their effective implementation.

The move to Harbourgate

13. The location of the BTI project at the Belfast City Hospital (BCH) site was seen as fundamental to the success of the project. Despite this, DETI and its agencies each approved the move to Harbourgate. Crucially, however, they did not carry out a re-appraisal of the project to confirm that it remained financially viable and that its strategic objectives remained deliverable at the new location. This was a major breach of procedures and one that led directly to the ultimate demise of the project. Further, they did not confirm that the Harbourgate building was physically suitable for use as a bioscience research and incubation facility — as it transpired, it was far from suitable. Moreover, when approving the purchase of Harbourgate, DETI and its agencies failed to ensure that the project was fully financed, even though this was a fundamental prior condition of the grant offer. As a result, the project was only two thirds funded, with a shortfall of some £2.7 million. This was clearly a recipe for disaster.

14. The Committee also noted that Invest NI's decision in 2002 to enter into a contract to buy the Top Floor of Harbourgate from BTI for £1.5 million, involved multiple breaches of its guidelines. There was no business case to justify the purchase, no contemporaneous record of the decision-making process and no written record of the Chief Executive's approval. These shortcomings were compounded by Invest NI's failure to obtain both DFP and ministerial approval for the contract. As regards the absence of documentation, two separate records, seeking to justify the contract, were prepared between three and eight months after the event. Neither was signed or dated and there were inconsistencies between the two documents. In the Committee's view, this whole episode demonstrates a staggering disregard for proper administration and the management of public money.

Amendments to Letters of Offer

15. DETI and Invest NI each amended their Letters of Offer to facilitate the earlier drawdown of grant by BTI. The reasons given were BTI's inability to meet offer conditions and to retrospectively allow ineligible expenditure already incurred and claimed by BTI. The Committee notes, however, that this weakened their control over the project and undermined the very purpose of the conditions of offer — to protect public money in the event of BTI failing to deliver. Moreover, DETI failed to obtain DFP approval to the amendments. The Committee also notes that, in order to spend grant monies before an impending funding deadline, DETI amended its offer to facilitate the purchase of over £350,000 of equipment by BTI. However, this was done at a time when the company did not even have premises to store, never mind operate the equipment. As it turned out, BTI never used the equipment and the money was wasted.

Recommendation 4

16. The conditions and prior conditions included in letters of offer are a direct response to the risks assessed at appraisal. The Committee recommends that any proposal to change those conditions, which significantly increases the risk to the funder, should be subjected to a formal re-appraisal before the decision is made.

Recommendation 5

17. The Committee recommends that DETI and Invest NI take steps to ensure that decisions to pay grant are not driven solely by the need to meet funding deadlines. While the Committee readily acknowledges the importance of such deadlines, no payment should be made if the provision of grant cannot otherwise be fully justified.

Project Monitoring

18. Project monitoring was a major area of weakness in the Department's handling of this project, at times being virtually non-existent. Examples of shortcomings, included:

- failure to follow-up the non-submission, by BTI, of quarterly and annual accounts and progress reports;

- failure to challenge the absence of BTI Board Minutes for the first 21 months of its existence;

- failure to validate the accuracy of data provided by BTI;

- failure to take full advantage of observer status on the BTI Board – an IDB/Invest NI representative attended only 13 of the 32 recorded Board meetings;

- failure to detect, until a very late stage, the difficulties and lack of progress in developing the project at the BCH site;

- failure to closely monitor BTI's fund-raising efforts, even though they were critical to the project's success.

The Committee notes that it was largely through the scrutiny of the private donor, rather than Invest NI's observer, that major concerns around BTI's standards of corporate governance, financial control and project management started to emerge. That is a damning example of how poorly this project was being monitored.

Recommendation 6

19. The Committee recommends that DETI and Invest NI review their project monitoring procedures to take on board the lessons from the BTI case. Grant-aided projects must always be actively monitored; where information provided by an assisted body is deficient, or indicates that the project is not proceeding to plan, this must be quickly addressed, including where necessary, a re-appraisal of the project.

Corporate Governance within BTI

20. The Department failed to ensure that proper standards of corporate governance were applied within BTI. Two of the main areas of concern were procurement and conflicts of interest. For example, contrary to the conditions of offer, BTI failed on almost every occasion to use selective tendering to procure goods and services. Despite this, every grant claim was authorised and paid.

21. There was no formal procedure within BTI for handling conflicts of interest. The evidence indicates that conflicts which did arise were generally poorly handled, with lack of disclosure a recurrent weakness. Many of the unresolved conflicts, involving certain Board Members and their close relatives, must have been obvious to senior management within DETI and its agencies, yet nothing was done to address them. One example which stands out particularly is the appointment of MTF Chartered Accountants to administer the start-up of BTI at a cost of some £68,000. This points towards a culture of "cronyism" within the upper echelons of IDB and a "cosy relationship" between DETI and one of its most prominent public appointees.

22. It is clear that both the BTI Board and DETI and its agencies placed a disproportionate amount of trust in Teresa Townsley, to the extent that their exercise of a challenge function fell far short of what might reasonably have been expected. This is not the first time that the Public Accounts Committee has advised against over-reliance on an individual within a major industrial development project. It is now time that this lesson is learned.

Recommendation 7

23. When providing substantial sums of financial assistance to organisations like BTI, DETI and Invest NI must ensure that comprehensive corporate governance structures are in place and are fully functional when the project starts. This must include ensuring that the Board itself possesses the appropriate range and level of skills and experience.

Payment of Claims

24. On two occasions, DETI disregarded its agreed funding procedures by paying grant claims when it was aware that the qualifying expenditure had not yet been incurred by BTI. The first instance involved a copy cheque for £1.7 million which was submitted by BTI as proof of payment towards the cost of Harbourgate; the second involved 11 copy cheques totalling some £350,000 for the purchase of equipment. However, on both occasions, the cheques had not actually been presented for payment and appear to have been written for the sole purpose of drawing down grant in advance, rather than as a means of settling invoices.

25. BTI also double-claimed some £542,000 from both DETI and IFI. As a result, the expenditure involved was grant-aided to the tune of 92%. Despite being alerted by IFI, DETI took no action. Although the Accounting Officer said that this level of grant assistance was permitted under EU funding guidance at that time, it is clear that it was not the intention of either DETI or IFI to both fund the same expenditure. DETI's failure to take action on this issue was a poor judgement, especially as, in presenting the IFI claim, BTI had falsely declared that the source of matching funding was "private sector" rather than DETI.

Recommendation 8

26. Bypassing agreed payment authorisation procedures and failing to ensure that conditions of offer have been met are serious breaches of control. The Committee recommends that the Department ensures its arrangements for releasing grants to projects are sufficiently rigorous to prevent payments being made until all relevant checks have been satisfactorily completed and all conditions of offer complied with.

27. There are a number of important lessons which emerge from the above paragraphs that must be taken on board. The Committee has noted the assurances from both the Department and Invest NI that lessons have been learned and that controls are better today than 10 years ago. While these assurances are welcome, it must not be forgotten that most of the shortcomings in this case stemmed from a failure to apply existing controls, rather than through an absence of controls.

28. Interestingly, neither DETI nor Invest NI could offer much in the way of explanation, as to how so many breaches of their control procedures could have occurred. In the Committee's view, it was weak management combined with an absence of effective leadership. What is required going forward, therefore, is a changed culture, particularly at top management level, if this type of scenario is to be avoided in the future. This issue is discussed further in the penultimate section of this report.

DETI's response to the failings in this case

Introduction

29. The C&AG's report details a number of areas where the evidence raises strong suspicions of fraudulent behaviour. These include the finder's fee; grant claims (with instances of double claiming, false declarations and non-presentation of cheques for payment); misrepresentations that tenants had been secured for Harbourgate; mishandling of payments and recoveries in connection with overseas travel; and impropriety in the procurement of a consultancy firm to carry out an economic appraisal.

DETI's response to suspected fraud and impropriety was not sufficiently comprehensive

30. The Committee has serious concerns about the way in which the Department responded to its suspicions of fraud and impropriety. Overall, it appears to have adopted a piecemeal approach, particularly in its consultations with the PSNI. In two of the areas, Harbourgate tenants and the procurement of the economic appraisal, concerns were not discussed at all with the police. It is not clear whether this was through oversight or an error of judgement. Concerns about overseas travel were discussed with the PSNI in 2005, but these discussions were described as "informal" and were held prior to the company inspection process which provided the hard evidence of wrongdoing. No subsequent discussion appears to have taken place.

31. As regards grant claims, the Department discussed its concerns with the police in 2010. However, PSNI commented that DETI, by its actions, had effectively consented to BTI engaging with the claims process in the manner in which it did. This included retrospectively amending its Letter of Offer to reflect expenditure that BTI had already incurred and claimed; taking no action on becoming aware of double claiming; and, contrary to the agreed funding procedures, releasing grant before all outstanding queries had been resolved.

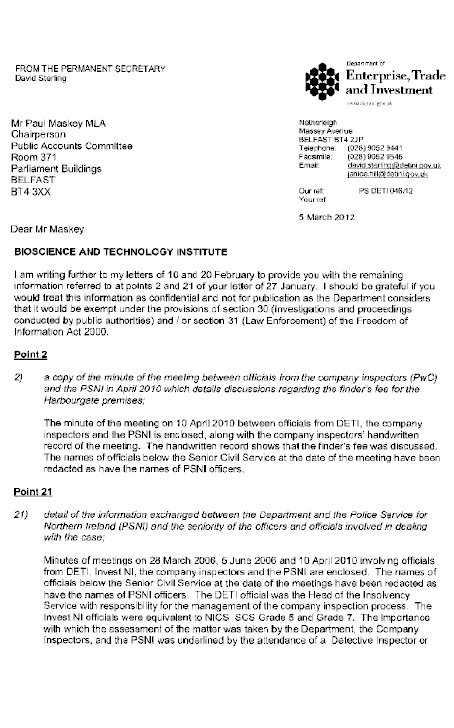

32. On the finder's fee, the Department discussed matters with the PSNI in 2006. However, this was at an early stage of the company inspection process, more than three years prior to its completion. At that time, it appears that PSNI's view was that there was insufficient evidence to take matters further in terms of criminal proceedings. While the C&AG was told that this was the only consultation with the police on the finder's fee issue, the Accounting Officer revealed at the hearing that evidence had just come to light of a further discussion with PSNI in 2010. Details were provided in follow-up correspondence.

33. It appears, however, that this further discussion involved no more than a brief exchange in the course of the meeting with PSNI on grant claims (paragraph 31 above). Indeed, the finder's fee issue was not even included in the formal minute of this meeting, which further indicates that the discussions were far from comprehensive. This is extremely disappointing, given the seriousness of the finder's fee issue. Moreover, the Committee finds it in no way reassuring to learn that the Accounting Officer was unaware of these discussions, however brief, until immediately before the hearing. The lack of communication within the Department on this issue is very worrying.

34. Overall, the Committee's view is that DETI should have dealt with the suspected fraud and impropriety on a holistic basis, formally consulting with the PSNI on all matters of concern after completion of the Company Inspectors' report and providing a comprehensive evidence pack for detailed consideration by the police. Fraud and impropriety, whether actual or attempted, are serious issues which this Committee expects Departments to address comprehensively and professionally, not in the haphazard fashion so evident in this case.

Recommendation 9

35. The Committee is critical of the haphazard way in which DETI responded to the suspicions of fraud and impropriety in this case, particularly in its consultations with the PSNI. The Committee recommends, therefore, that DETI reviews the adequacy of its fraud response plan, considers whether additional training is required for staff charged with handling fraud cases and reports back to the Committee with its conclusions and recommendations for improvement.

The acquisition of Harbourgate

36. The Committee is far from convinced that it has got to the bottom of the circumstances surrounding the acquisition of the Harbourgate building. The lack of transparency around the sourcing of the premises and the negotiation of the purchase price is deeply disturbing — there are no contemporaneous written records of the process. However, based on interview evidence gathered by the Company Inspectors, the following is understood:

- Harbourgate was apparently sourced by an independent property dealer working on behalf of BTI. He had been engaged by Thomas Armstrong, BTI's solicitor. However, with the exception of Teresa Townsley, no-one else on the BTI Board was aware of the property dealer's identity or role. Consequently, no instructions were given to the property dealer by the BTI Board. Nor is there any indication as to whether he was suitably qualified to act in this capacity.

- Whereas the property dealer was not known to the BTI Board, he and the vendor had been known to one another for many years.

- Despite the absence of instruction from the BTI Board, the property dealer negotiated a price of £5 million for Harbourgate with the vendor. However, this was done without a formal, independent valuation of the building and no indication of its market value, as the property was not being actively marketed and never had been. Even more bizarrely, the property dealer told the Company Inspectors that he had not been given a budget figure for the negotiations. Coincidentally, however, the purchase price which he negotiated with the vendor was the same as the available funds in BTI (£5 million).

- The building had been developed by the vendor as a call centre for a particular tenant. However, that tenant had not proceeded with the arrangement and, at the time of the BTI purchase, no other tenant or buyer had been secured. In such circumstances, it might reasonably be expected that a keen price could have been negotiated, in what was arguably a buyer's market. Interestingly, however, in the course of their work, the Company Inspectors calculated that the sale of the Harbourgate building to BTI yielded the vendor an overall gain in the region of £2.3[1] million before tax. This does not suggest any sense of hard bargaining in the negotiations.

In light of the above, the Committee is far from assured that the acquisition of Harbourgate was conducted at arm's length and in good faith.

Recommendation 10

37. The Committee recommends that DETI rigorously investigates the circumstances surrounding the sourcing of the Harbourgate building and negotiation of the purchase price, and then consults with the PSNI to determine whether any criminal actions may have taken place, and informs the Committee of the outcome.

DETI has instituted Director Disqualification proceedings against one former Director of BTI

38. The Department has recently initiated director disqualification proceedings against one of the former directors of BTI, Teresa Townsley. In light of the evidence presented in the C&AG's report, the Committee welcomes this course of action. As the BTI company secretary, she was responsible for corporate administration and for ensuring that BTI complied with regulatory requirements, both legal and financial.

39. The Committee notes that this is not the first occasion on which concerns surrounding the conduct of Mrs Townsley have been reported. In 2006, the Westminster Public Accounts Committee reported on its examination of the 'Emerging Business Trust'[2], stating that every one of Lord Nolan's principles of public life had been breached and describing it as one of the worst cases of conflict of interest and impropriety it had seen. However, the Department failed to take any disqualification action against Mrs Townsley on that occasion.

40. The Department said that all former BTI directors were examined regarding the merits of disqualification proceedings. However, when the public interest test was applied, it was concluded that only Mrs Townsley should be subjected to proceedings. The Committee acknowledges the Department's comments but notes that, although the other parties in the project may have taken assurance from Mrs Townsley's involvement, given her experience and standing within the Department at that time, the directors as a whole were responsible for corporate governance. The Committee also notes that the funding bodies themselves had an important role to ensure that standards were met, but failed to do so.

Referrals to professional Bodies

41. The Department, in conjunction with DFP, also referred concerns about the conduct of four individuals to their professional bodies, about actions which they considered may have breached professional codes of conduct. Three of the referrals were to the 'Chartered Accountants Regulatory Board' (CARB). Of these, the cases of Teresa Townsley and Michael Townsley are still under consideration by CARB. The third case involved FPM Chartered Accountants and one of its directors, who were referred in relation to concerns over a serious conflict of interest in the award to FPM, by BTI, of a contract to carry out an economic appraisal.

42. CARB concluded that the evidence was not sufficient to ensure that a complaint had any real prospect of being established before a Disciplinary Tribunal. This decision was upheld on appeal by an Independent Reviewer of Complaints engaged by CARB. The Committee notes that, in his analysis, the Independent Reviewer drew attention to:

- the lapse of time, of over 10 years, between the events which led to the referral and the date of the referral itself. In his view, this delay was both inordinate and inexcusable and gave rise to the substantial risk of serious prejudice to the Member (the FPM director);

- his opinion that the Complainant (DFP and DETI) failed to comment on, let alone explain, how a conflict of interest had actually arisen in the case.

43. The Committee notes CARB's decision but is disappointed with the outcome. It is also disappointing that the referral by DFP and DETI was judged not to have presented the complaint in a clear and comprehensive manner. Referrals to professional bodies require the highest standard of presentation if they are to be successful.

Recommendation 11

44. The Committee recommends that DETI and DFP ensure that future referrals to professional bodies are processed on a much more timely basis and that the substance of the complaint is fully and clearly articulated.

45. The other referral was to the Law Society of Northern Ireland, regarding the conduct of Thomas Armstrong, BTI's solicitor, in the sourcing and acquisition of Harbourgate. The Committee was astonished to learn that the Law Society had accepted Mr Armstrong's explanations on these matters. In the circumstances, the Committee is disappointed that the Department did not appeal the Law Society's decision, or even enter into discussion with them to ascertain the rationale for their decision.

Recommendation 12

46. The Committee recommends that DETI clarifies with the Law Society the rationale behind its decision to accept the explanation of BTI's solicitor.

Disciplinary proceedings against officials

47. The Department commissioned an independent review of the conduct of officials involved in the BTI case. The position of four officials was examined and this resulted in disciplinary action being taken by Invest NI against two of its officers, in February 2011. In the case of the other two officials reviewed — a former Chief Executive of IDB from 1995 to November 2000 and a middle-ranking manager in DETI at the material time — no disciplinary action was taken. Details of both cases were provided to the Committee, by the Accounting Officer, after the Evidence Session.

48. The review of the conduct of the former IDB Chief Executive was based on his failure to ensure that the BTI project was assessed through a Casework Committee process. Instead it had been taken to the IDB Resource Group, an inappropriate mechanism and one which involved a much lower level of scrutiny (paragraph 7 above). The Accounting Officer said that in assessing the case, he had taken advice from his human resources department and from the Permanent Secretary of DFP; he had also consulted the departmental solicitor. Following careful consideration of the advice provided, he had concluded that the commencement of formal disciplinary proceedings would not be warranted. Given that the failure to examine the BTI project through the required Casework Committee process was a serious and fundamental breach of IDB procedures, the Committee finds it difficult to accept this conclusion.

49. While the Department is to be commended for instigating a disciplinary process, the Committee has a concern about the extent to which that process was applied. The conduct of only four officials was examined, whereas the failings in this case ranged much more widely. For example, contrary to the rules:

- senior officials within DETI and IDB approved BTI's move to Harbourgate without insisting on a full re-appraisal of the project and despite the existence of a £2.7 million funding gap that could not be met. Moreover, they failed to obtain DFP approval

- senior officials within Invest NI approved entering into a contract to purchase the Top Floor of Harbourgate from BTI for £1.5 million, without preparation of a Business Case and without seeking DFP and ministerial approval.

These were fundamental breaches of procedures that put large sums of taxpayer's money at substantially increased risk.

50. The Committee notes the Accounting Officer's explanation that the disciplinary review did not consider the conduct of retired departmental and Invest NI employees, because they are now effectively beyond the reach of the disciplinary processes. In the Committee's view, it is most unfortunate that several of those officials seemingly most culpable for the shortcomings in this case could not be subject to a disciplinary investigation, by virtue of their having retired from the public sector. This renders the outcome of the disciplinary process less than satisfactory.

Recommendation 13

51. The Committee recommends that the Civil Service ensures that disciplinary issues, in cases like BTI, can be dealt with much more urgently.

The failure of leadership within the Department and its agencies

There were serious lapses at a senior level within both IDB/Invest NI and DETI

52. It will be clear from the earlier sections of this report that one of the issues which the Committee has found most disturbing in the BTI project is the extent to which some of the most senior officials in both DETI and IDB/Invest NI were apparently complicit in the many failings that occurred. The Committee's impression is of a management culture at that time which ignored the rules, set aside crucial lessons from earlier projects and circumvented their own controls. That is an appalling indictment. Whether these lapses stemmed from apathy, incompetence or simply a disregard for the proper conduct of public business, they are wholly unacceptable.

53. The Committee acknowledges that the effective oversight of a major new innovation project presents many challenges. But it is precisely because of the numerous risks involved, that the successful handling of such a project requires not only the highest standards of administration, but also a commensurate standard of leadership. One of the most important messages coming out of this report, therefore, is to stress the particular onus on an organisation's top management to ensure that control procedures are followed and that the ethos of their organisation is fully in keeping with the proper conduct of public business.

54. The Committee notes the work being done within Invest NI by the current Chief Executive through his 'Transform' programme of change and commends him for this initiative. It is important that both Invest NI and DETI now ensure that the lessons from the BTI project are assimilated within their respective organisations.

Recommendation 14

55. There is a particular responsibility on top management to encourage a culture of compliance with good practice throughout their organisation. The Committee recommends that both DETI and Invest NI now ensure that the lessons on leadership and management culture arising from the report are assimilated within their respective organisations.

Project Outcomes

The project failed to achieve any of its objectives

56. The Committee is extremely disappointed with the outcomes of this project. Through a combination of negligence, incompetence and a disregard for proper administration, the bioscience research and incubation facility was never established. As a result, an initiative that promised so much and which should have been a major success story for Northern Ireland was instead transformed into an unmitigated failure.

57. The demise of this project was a significant loss to the local economy, in that this type of facility was likely to have underpinned a substantial level of development in new and emerging companies, in a sector where considerable growth potential was forecast. Indeed, target outcomes for the project included the creation of 10 new start-up companies within five years, with jobs for 50 Northern Ireland graduates, and six new inward investors.

58. In view of the project failing to achieve any of its objectives, the Committee can only conclude that it provided no value for the public funds committed to it. Further, with no sums having been recovered by Government, some £2.2 million of taxpayers' money has been totally wasted. In addition, over £1 million is also left owing to the estate of the private donor and a further £0.4 million is owed to HM Revenue and Customs. This is a devastating ending to a venture that had so much potential.

The subsequent use of the Harbourgate building

59. Although the subsequent use of the Harbourgate building was not the focus of this inquiry, the Committee noted that, following Invest NI's decision to exit from the project in 2003, the Harbourgate building was sold to a private development company in 2005. Shortly thereafter, DFP entered into a tenancy agreement with the development company to rent the premises for a period of 15 years at a total cost of almost £11 million. The Committee recognises that there are various factors to be considered in assessing the value for money of such an arrangement. However, given that the building as a whole could have been acquired from BTI for less than half that sum, the Committee is concerned that a more advantageous deal for taxpayers might have been possible before the sale of the building to the private development company.

[1] The Committee understands that the £2.3 million figure includes a non-taxable sum of some £1.3 million subsequently channelled through an option release mechanism set up in the Isle of Man.

[2] Governance issues in the Department of Enterprise, Trade and Investment's former Local Enterprise Development Unit', Forty-sixth Report of Session 2005-06, HC 918. EBT was a publicly funded loan and venture capital initiative set up by the Department to assist in financing emerging businesses in disadvantaged areas.

Appendix 1

Minutes of Proceedings

of the Committee

Relating to the Report

Wednesday, 11 January 2012

Room 29, Parliament Buildings

Present: Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

In Attendance: Ms Aoibhinn Treanor(Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: Mr Paul Maskey MP (Chairperson)

Ms Jennifer McCann

Mr Adrian McQuillan

2:01 pm The meeting opened in public session.

4. Briefing on the NIAO Report on 'Bioscience Technology Institute Ltd'

Mr Kieran Donnelly, Comptroller and Auditor General; Mr Robert Hutcheson, Director; and Mr Roger McCance, Senior Auditor; briefed the Committee on the report.

3:09 pm The meeting went into closed session after the C&AG's initial remarks.

3:34 pm Mr Girvan left the meeting.

3:37 pm Mr Girvan entered the meeting.

3:42 pm Mr Copeland left the meeting.

3:43 pm Mr Hussey left the meeting.

3:50 pm Mr Copeland entered the meeting.

4:02 pm Mr Dallat left the meeting.

4:08 pm Mr Dallat entered the meeting.

The witnesses answered a number of questions put by members.

[EXTRACT]

Wednesday, 18 January 2012

Room 29, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Ms Jennifer McCann

Mr Mitchel McLaughlin

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: Mr Ross Hussey

Mr Adrian McQuillan

2:03 pm The meeting opened in public session.

4. Evidence on the Northern Ireland Audit Office Report 'DETI: The Bioscience Technology Institute'.

The Committee took oral evidence on the above report from:

- Mr David Sterling, Accounting Officer, Department of Enterprise, Trade, (DETI);

- Mr Trevor Cooper, Head of Finance, Department of Enterprise, Trade, (DETI);

- Mr Alastair Hamilton, Chief Executive, Invest NI; and

- Mr Mel Chittock, Executive Director, Invest NI.

3.15 pm Mr Copeland left the meeting.

3.18 pm Mr Copeland entered the meeting.

4.10 pm Mr Girvan left the meeting.

4.11 pm Mr Girvan entered the meeting.

4.20 pm Ms McCann left the meeting.

4.35 pm Ms McCann entered the meeting.

4.35 pm Mr Dallat left the meeting.

4.38 pm Mr Byrne left the meeting.

4.40 pm Mr Dallat entered the meeting.

4.41 pm Mr Byrne entered the meeting.

4.54 pm Mr Copeland left the meeting.

4.55 pm Mr Copeland entered the meeting.

4.58 pm Ms McCann left the meeting.

5.10 pm Mr Byrne left the meeting.

5.37 pm Mr Easton left the meeting.

The witnesses answered a number of questions put by the Committee.

Agreed: The Committee agreed to request further information from the witnesses.

[EXTRACT]

Wednesday, 25 January 2012

Room 29, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Mitchel McLaughlin

Mr Adrian McQuillan

Mr Conor Murphy MP

In Attendance: Ms Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Ms Angela Kelly (Assembly Legal Services)

Apologies: Mr Ross Hussey

2:02 pm The meeting opened in public session.

2:46 pm The meeting went into closed session.

6. Issues arising from the oral evidence session on NIAO 'Bioscience Technology Institute'

The Committee considered an issues paper on this evidence session.

4:09 pm Mr McQuillan left the meeting.

4:22 pm Mr Copeland left the meeting.

A member suggested that the Committee cross-reference serious breaches by officials in successive reports of the Committee over a defined term, to identify legacy and succession issues.

Agreed: The Committee agreed to consider options on this approach.

[EXTRACT]

Wednesday, 1 February 2012

Room 29, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Mitchel McLaughlin

Mr Conor Murphy MP

Mr Adrian McQuillan

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: Mr Ross Hussey

2:01 pm The meeting opened in public session.

3. Matters Arising

Correspondence re Bioscience Technology Institute

The Committee noted correspondence sent anonymously highlighting concerns over the level of oversight of the Bioscience Technology Institute following the Committee's evidence session on 18 January 2012.

A member advised the Committee that they were also in receipt of correspondence from a whistleblower pertaining to the Committee's inquiry.

Agreed: The Committee agree to forward the information raised to the Comptroller and Auditor General to investigate the issues and report back to the Committee.

[EXTRACT]

Wednesday, 22 February 2012

Room 29, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Adrian McQuillan

Mr Conor Murphy MP

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: Mr Ross Hussey

Mr Mitchel McLaughlin

2:00 pm The meeting opened in public session.

6. Correspondence received relating to the Committee's Inquiry into 'DETI: The Bioscience Technology Institute'

3:10 pm Mr McQuillan entered the meeting.

3:21 pm Mr Anderson entered the meeting.

The Committee noted correspondence from Mr David Sterling, Accounting Officer, Department of Enterprise, Trade and Investment providing further information for its inquiry.

[EXTRACT]

Wednesday, 29 February 2012

Room 29, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

Mr Adrian McQuillan

Mr Conor Murphy MP

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mr Gavin Ervine (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: Mr John Dallat

2:00 pm The meeting opened in public session.

2:01 pm Mr Copeland entered the meeting.

2:09 pm Mr McLaughlin declared an interest stating that he is a pensioner.

2:11 pm Mr Girvan entered the meeting.

2:15 pm The meeting went into closed session after the C&AG's initial remarks.

2:38 pm Mr Hussey left the meeting.

2:41 pm Mr Copeland and Mr Easton left the meeting.

2:43 pm Mr Copeland and Mr Easton entered the meeting.

2:59 pm Mr Murphy left the meeting.

3:02 pm Mr Easton and Mr Girvan left the meeting.

3:07 pm Ms Kelly from Assembly Legal Services joined the meeting to advise the Committee as client in confidence. External advisers left the meeting.

3:16 pm Mr Easton and Mr Girvan entered the meeting.

3:22 pm Mr Byrne left the meeting.

3:24 pm Mr Girvan left the meeting.

3:25 pm Mr Byrne entered the meeting.

3:25 pm Ms Kelly left the meeting.

3.35 pm External advisers rejoined the meeting.

6. Consideration of Draft Committee Report on 'The Bioscience and Technology Institute'

The Committee considered the first draft of its report on 'Bioscience and Technology Institute'

Paragraphs 1 - 7 read and agreed.

Paragraph 8 read, amended and agreed.

3:55 pm Mr Anderson left the meeting.

Paragraph 9 read and agreed.

Paragraph 10 read, amended and agreed.

Paragraphs 12 -13 read and agreed.

4:06 pm Mr Anderson entered the meeting.

Paragraph 14 read, amended and agreed.

Paragraphs 15 – 18 read and agreed.

Paragraph 19 deferred for further consideration.

Paragraphs 20 – 23 read and agreed.

Paragraph 24 read, amended and agreed

Paragraph 25 read and agreed.

Paragraph 26 read, amended and agreed.

Paragraphs 27 – 29 read and agreed.

Paragraph 30 read, amended and agreed.

Paragraph 31 read and agreed.

4:14 pm Mr McQuillan left the meeting.

Paragraph 32 deferred for further consideration.

Paragraphs 33 - 34 read, amended and agreed.

Paragraph 35 read, amended and agreed.

Paragraph 36 deferred for further consideration.

Paragraph 37 read, amended and agreed.

Paragraph 38 read and agreed.

Paragraph 39 read, amended and agreed.

Paragraphs 40 – 43 read and agreed.

Paragraph 44 read, amended and agreed.

Paragraphs 45-46 read and agreed.

Paragraphs 47 – 53 deferred subject to further advice.

Paragraph 53(b) read and agreed.

Paragraphs 54 – 55 read, amended and agreed.

Paragraphs 56 – 57 read and agreed.

Paragraph 58 – 59 read, amended and agreed.

Agreed: The Committee agreed to write to the Department to clarify some information.

3:25 pm Mr Murphy left the meeting.

[EXTRACT]

Wednesday, 14 March 2012

The Senate Chamber, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

Mr Adrian McQuillan

Mr Conor Murphy MP

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Apologies: None

2:00 pm The meeting opened in public session.

2:03 pm Mr Murphy entered the meeting.

2:05 pm Mr McQuillan entered the meeting.

2:21 pm The meeting went into closed session.

7. Committee's Inquiry 'Bioscience and Technology Institute'

The Committee noted correspondence from Mr David Sterling, Accounting Officer, Department of Enterprise, Trade and Investment providing additional information requested by the Committee.

[EXTRACT]

Wednesday, 21 March 2012

The Senate Chamber, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

Mr Conor Murphy MP

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mrs Danielle Saunders (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

Mr Jonathan McMillen (Assembly Legal Services)

Apologies: Mr Joe Byrne (Deputy Chairperson)

Mr John Dallat

Mr Adrian McQuillan

2:02 pm The meeting opened in public session.

6. Draft Committee Report on 'Bioscience Technology Institute'

Correspondence from the Department of Enterprise, Trade and Investment

The Committee noted correspondence from Mr David Sterling, Accounting Officer, Department of Enterprise, Trade and Investment detailing legal processes the Department is engaged in and providing a holding reply to the Committee's further request for information.

2:21 pm The meeting went into closed session.

2:21 pm Mr McMillen from Assembly Legal Services joined the meeting to advise the Committee as client in confidence. External advisors left the meeting.

The Committee were briefed by Mr McMillen on the legal advice sought in relation to its draft report.

2:24 pm Mr Girvan entered the meeting.

2:30 pm Mr Murphy left the meeting.

2:31 pm Mr Hussey left the meeting.

2:35 pm Mr Hussey entered the meeting.

This was followed by a question and answer session.

Agreed: The Committee agreed to give further consideration to its draft report, reflecting the advice received, at a future meeting.

2:46 pm Mr McMillen left the meeting.

[EXTRACT]

Wednesday, 2 May 2012

The Senate Chamber, Parliament Buildings

Present: Mr Paul Maskey MP (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Mr Ross Hussey

Mr Mitchel McLaughlin

Mr Adrian McQuillan

Mr Conor Murphy MP

In Attendance: Miss Aoibhinn Treanor (Assembly Clerk)

Mr Phil Pateman (Assistant Assembly Clerk)

Mr Gavin Ervine (Clerical Supervisor)

Mr Darren Weir (Clerical Officer)

2:02 pm The meeting opened in public session.

6. Draft Committee Report on Bioscience Technology Institute

The Committee gave further consideration to its draft report.

3:21 pm Mr Murphy left the meeting.

3:27 pm Mr Copeland left the meeting.

3:30 pm Mr Copeland and Mr Murphy entered the meeting.

3:30 pm Mr Anderson, Mr Girvan and Mr Hussey left the meeting.

3:31 pm Mr Easton entered the meeting.

3:32 pm Mr Anderson entered the meeting.

3:44 pm Mr Copeland left the meeting.

3:45 pm Mr Copeland and Mr Girvan entered the meeting.

Paragraphs 1, 19, 24, 28 and 32 read and agreed.

Paragraph 33 read, amended and agreed.

Paragraphs 43, 45, 46 read and agreed.

3:47 pm Mr Murphy left the meeting.

Paragraph 47 read and agreed.

3:46 pm Mr Murphy entered the meeting.

Paragraph 48 read, amended and agreed.

Paragraphs 49 – 51 read and agreed.

Paragraph 52 read, amended and agreed.

Paragraphs 53, 55, 56 and 60 read and agreed.

Consideration of the Executive Summary

Agreed: The Committee agreed to reflect the amendments to the body of the report in the Executive Summary.

4:15 pm Mr Dallat left the meeting.

4:17 pm Mr Murphy left the meeting.

Agreed: The Committee considered a correspondence schedule from the Clerk and agreed the correspondence to be included within the report.

Agreed: The Committee ordered the report to be printed.

[EXTRACT]

Appendix 2

Minutes of Evidence

18 January 2012

Members present for all or part of the proceedings:

Mr Paul Maskey (Chairperson)

Mr Joe Byrne (Deputy Chairperson)

Mr Sydney Anderson

Mr Michael Copeland

Mr John Dallat

Mr Alex Easton

Mr Paul Girvan

Ms Jennifer McCann

Mr Mitchel McLaughlin

Witnesses:

|

Mr Trevor Cooper |

Department of Enterprise, Trade and Investment |

|

|

Mr Mel Chittock |

Invest NI |

Also in attendance:

|

Mr Kieran Donnelly |

Comptroller and Auditor General |

|

|

Ms Fiona Hamill |

Treasury Officer of Accounts |

1. The Chairperson: Agenda item 4 is the evidence session on the Audit Office report, 'DETI: The Bioscience and Technology Institute'. Does any member wish to express an interest in the matter?

2. I welcome Mr David Sterling, accounting officer for the Department of Enterprise, Trade and Investment (DETI), who is here to respond to the Committee. Members, you will be aware that the Department has provided some more information, which you have in front of you. That is most irregular for the Committee.

3. Mr Sterling, perhaps you could introduce your colleagues and then explain why we have this additional information.

4. Mr David Sterling (Department of Enterprise, Trade and Investment): Thank you, Chair. Joining me today is Mr Alastair Hamilton, chief executive of Invest Northern Ireland; Mr Mel Chittock, executive director of finance and internal operations in Invest NI; and Mr Trevor Cooper, head of finance in DETI.

5. I regret the way in which the additional information had to be brought to the Committee. It was a document that we and the Audit Office had seen, but I suspect that we had not realised that it might be germane to some of today's discussions. I apologise for the late notification of the information. It only became apparent in the last day or so that it was a matter of interest.

6. The Chairperson: OK. I take you to the back page of that information, which relates to informal conversations with the PSNI. However, with regard to the second paragraph, which relates to the finder's fee, are there minutes of the discussions between yourselves, the Department, the PSNI and whoever else was involved?

7. Mr Sterling: The significance of the document that we are bringing to your attention is that it indicates that there had been some discussion with the police in 2004 about the double claiming of travel claims. I think that that is correct.

8. Mr Trevor Cooper (Department of Enterprise, Trade and Investment): Yes.

9. Mr Sterling: Neither ourselves nor the Audit Office had been clear, up to this point, that the issue of the travel claims had been brought to the attention of the PSNI. That is the only reason why we brought the document to the Committee's attention today.

10. The Chairperson: The second paragraph of the e-mail that the Committee has just seen relates to the finder's fee. That is why I am saying that it is very irregular for this to happen to the Committee. Even though some reports were done after 2004, I note that the letter was written in 2005. There were reports after that — right up to 2010. Are there minutes of those meetings to say what discussions took place with the PSNI and the results of those discussions?

11. Mr Sterling: Yes, there are minutes of the three meetings that took place between the company inspectors, Invest NI and the Department. I think that I am right in saying that minutes of those meetings were produced in DETI or Invest NI. PricewaterhouseCoopers (PwC) said that it has a note of its meeting referred to in the e-mail, and it is prepared to provide us with that if the Committee requests it.

12. Mr Cooper: We will ask for that information if the Committee requests it.

13. The Chairperson: We are requesting it. I will ask members and, hopefully, we will agree at the end of the meeting to request that information. Is the finder's fee mentioned in the PwC minutes?

14. Mr Cooper: PwC has confirmed that that is the case.

15. The Chairperson: It has confirmed that with you. We look forward to seeing that report.

16. Mr Copeland: My question is related but slightly askance. The responsibility to pursue a prosecution does not reside with the police. The police's responsibility is to gather the evidence and prepare a file. That file may then be forwarded to the Public Prosecution Service with or without a recommendation. For me to have any confidence in this, I would need to know what the police were told, who was told and the official view that came back. Is what you have just said evidence, or does it indicate that a paper trail exists about what was communicated to the police? What was asked of the police, what was the opinion that they subsequently gave and what was the rank of the person who was spoken to?

17. Mr Sterling: We have minutes that indicate the rank of the police officers who were at each of the three meetings, so we know who they were. The notes of those meetings give an overview of the discussions that took place. However, the minutes do not record everything that was said or every document that was discussed. We are working on the basis that, in a matter that could provide evidence of criminal intent, our responsibility is such that the company inspectors would bring that to the attention of the PSNI. The PSNI would then make a judgement on whether there was sufficient evidence for them to make a case to the Public Prosecution Service. In that regard, they are looking to be satisfied that there is something that would be beyond reasonable doubt or, in other words, would provide 99% certainty that a successful case could be mounted.

18. Mr Copeland: There are three tests, and one of those is the public interest. We can come back to that later, Chairperson.

19. The Chairperson: I appreciate that. You have told us that the finder's fee is mentioned in some of the minutes. You have the minutes to prove that. That is something that we would be looking for. Anything else, we can clarify with you in writing after today's session.

20. I will start by stating the very obvious. The report on the Bioscience and Technology Institute (BTI) makes for very unhappy reading. We can all agree with that. It catalogues a string of poor judgements, a failure by the funding bodies to apply many of their own guidelines and a disregard for key lessons from previous cases that the old Department had dealt with. What is your view of the way in which this case was handled by your Department and its agencies? Many of us have lobbied different Departments and arm's-length bodies to get investment into our own communities, areas and constituencies. Sometimes, you can hit your head off a brick wall in trying to get investment in, because there are that many obstacles to climb. In this particular case, having looked through the Audit Office report, it seems to me that a lot of obstacles were there but were broken or put aside and the project was pushed on with. That is not right. Maybe you can give us some explanation of all that.

21. Mr Sterling: Thank you, Chair. I welcome the opportunity to answer the Committee's questions on the reasons for the very regrettable failure of this project, which led to the loss of £2·2 million of taxpayers' money. For the record, I am happy to offer an apology on the part of the Department for any failings on its part that gave rise to that. We have already introduced many improvements to our governance arrangements since the event occurred. I am confident that the risk of this happening now is extremely low. I am happy to go through the changes and improvements that have been put in place. I am not sure whether you want to pick up on that now or later, but, certainly, the key point is that lessons have been learnt. We accept all the recommendations that the Comptroller and Auditor General has made, and will take careful account of any further suggestions that the Committee may wish to make.

22. I will pause there. I am not sure whether you want me to go into some more detail about what we have done since then.